Portfolio construction is about creating a disciplined, systematic framework that aligns with who you are as an investor, what you're trying to achieve, and how much volatility you can stomach on the journey.

This comprehensive guide will walk you through the fundamental principles of asset allocation, introduce you to different investor personas, and make a compelling case for why global diversification should be a cornerstone of every serious investment portfolio.

Table of Contents

- Understanding Asset Classes

- Portfolio Theory

- Matching Allocation to Identity

- The Case for Global Diversification

- Building Your Global Portfolio

Understanding Asset Classes

Before we dive into persona-based allocation, let's establish a clear understanding of the primary asset classes that form the building blocks of any investment portfolio:

Equities (Stocks)

- Purpose: Long-term capital appreciation and growth

- Risk Profile: High volatility, higher return potential

- Time Horizon: Best suited for long-term investors (7+ years)

Equities represent ownership in companies and historically have delivered the highest returns among major asset classes over extended periods. However, this comes with substantial short-term volatility. Drawdowns of 20-40% are not uncommon during market corrections.

Fixed Income (Bonds)

- Purpose: Income generation, capital preservation, and portfolio stability

- Risk Profile: Lower volatility, more predictable returns

- Time Horizon: Suitable for all time horizons depending on bond duration

Bonds provide regular income through interest payments and traditionally serve as a ballast against equity volatility. The bond market is roughly $145.1 trillion globally (as of 2024), providing ample diversification opportunities.

Commodities

- Purpose: Inflation hedge and portfolio diversification

- Risk Profile: High volatility, low correlation with stocks and bonds

- Time Horizon: Tactical allocations, cyclical exposure

Commodities including energy, metals, and agricultural products tend to perform well during inflationary periods and can provide crucial diversification during equity bear markets.

Cash

- Purpose: Liquidity, opportunity capital, and capital preservation

- Risk Profile: Lowest risk, lowest return

- Time Horizon: Immediate to short-term (0-2 years)

While cash doesn't offer meaningful returns in low-interest environments, it provides optionality and dry powder for opportunistic deployments during market dislocations.

The Evolution of Portfolio Theory

The concept of strategic asset allocation traces its roots to Harry Markowitz's Modern Portfolio Theory (MPT) developed in the 1950s. MPT introduced the revolutionary idea that investors should focus on portfolio-level risk and return rather than individual securities.

The Classic 60/40 Portfolio

The 60% equity / 40% bond allocation became the institutional standard in the post-1980 era, benefiting from:

- Falling interest rates: The 40-year bond bull market from 1981-2021 provided consistent gains

- Negative stock-bond correlation: Bonds zigged when stocks zagged, offering reliable diversification

- Disinflation regime: Stable, declining inflation supported both asset classes

However, the 2022 inflation shock and subsequent regime change exposed the vulnerabilities of this framework. When stocks and bonds fell simultaneously—the S&P 500 dropped 18% while the Bloomberg Aggregate Bond Index fell 13%—the 60/40 portfolio suffered its worst year since 1937, declining 17.5%.

This doesn't mean 60/40 is dead, but it underscores the importance of understanding why certain allocations work and adapting them to current market regimes and individual circumstances.

Investor Personas: Matching Allocation to Identity

| Conservative | Moderate | Balanced | Aggressive | |

|---|---|---|---|---|

| Equity | 15% | 30% | 40% | 70% |

| Fixed Income | 60% | 50% | 40% | 10% |

| Alternatives | 5% | 10% | 15% | 15% |

| Cash | 20% | 10% | 5% | 5% |

What Really Matters

While these persona frameworks provide useful starting points, it's critical to understand that they're not rigid prescriptions. Your actual allocation should consider:

- Human Capital vs. Financial Capital: A young doctor with stable, high future earnings can afford more equity risk than a commissioned salesperson of the same age.

- Goals-Based Allocation: Different goals require different portfolios. Your house down payment fund (2 years) should be allocated very differently from your retirement portfolio (30 years).

- Behavioral Resilience: The "right" allocation is one you can stick with during market turbulence. A 90% equity portfolio that causes you to panic-sell during a 30% drawdown is worse than a 60% allocation you maintain through the cycle.

Example

Profile: Supposed you are a mid-30s Indian professional or businessperson with a net worth of ₹4 Crores and a moderately high risk appetite. You reside in a Tier 1 city and frequently travel abroad for business or leisure.

Scenario: You have a high income with moderate to high stability. While your cash flow is consistent, your wealth is currently highly exposed to the Indian economy through your existing domestic investments and professional interests.

Goal: You seek moderate growth to build long-term wealth while establishing a "safety net" against local currency depreciation and domestic market concentration.

Recommended Allocation:

- 40% Indian Equities (₹1.6 Crore): Targeted exposure to domestic growth through a core of large-cap stability and a satellite of mid-cap alpha.

- 20% Global Equities (₹80 Lakhs): Strategic allocation to USD-denominated assets (e.g., S&P 500 or Global Tech). This ensures a significant portion of your wealth compounds in a hard currency.

- 30% Fixed Income (₹1.2 Crore): High-quality corporate bonds and debt instruments to provide a volatility buffer and capital preservation.

- 10% Alternatives & Cash (₹40 Lakhs): Divided between Gold (5%) for tail-risk protection and Liquid funds (5%) to maintain agility for market opportunities.

For an investor with a global lifestyle, a 20% international allocation is a functional necessity. By holding ₹80 Lakhs in global markets, you hedge against the consistent depreciation of the Rupee.

This protects your purchasing power for international expenses like frequent travel and future foreign education while providing ownership in sectors like Semiconductors and AI that are underrepresented in Indian indices.

The Case for Global Diversification

The Home Bias Problem

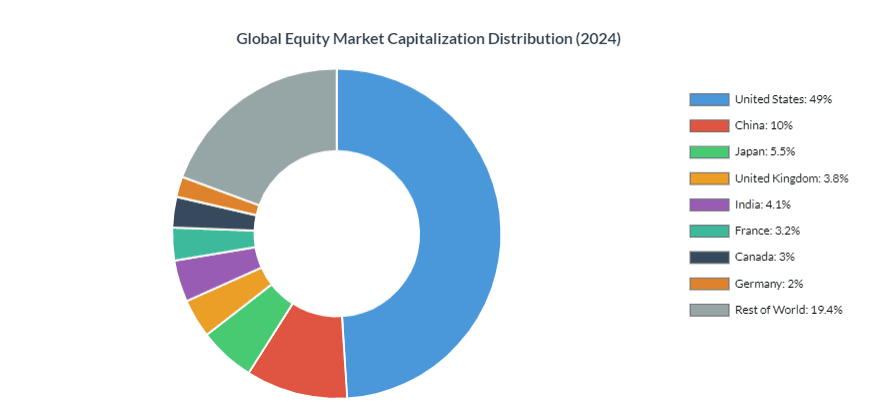

Home bias refers to investors' tendency to overweight domestic assets in their portfolios relative to what would be optimal from a diversification perspective. This is a global phenomenon, but it's particularly acute in India.

According to S&P Dow Jones Indices research, Indian investors allocate approximately 0.5% of their portfolios to international equities; essentially zero. This is one of the lowest rates globally, despite India representing only about 4% of global market capitalization.

Why Global Diversification Matters

1. Concentration Risk Reduction

By investing exclusively in Indian equities, you're essentially making a concentrated bet on:

- India's macroeconomic performance

- The rupee's stability against major currencies

- Indian regulatory and political environment

- Specific sector compositions dominant in Indian markets

No matter how optimistic you are about India's growth story, this concentration exposes you to significant idiosyncratic risk.

2. Access to Global Innovation & Leaders

Many of the world's most innovative companies and dominant industry leaders are not available on Indian exchanges:

- Technology: Apple, Microsoft, Google, Amazon, NVIDIA, Tesla

- E-commerce & Digital: Meta, Netflix, Shopify

- Healthcare & Biotech: Johnson & Johnson, Moderna, Pfizer

- Industrial & Aerospace: Boeing, Lockheed Martin, General Electric

These companies drive global consumption patterns, yet Indian investors have no direct access without global allocation.

3. Currency Diversification

The Indian rupee has depreciated consistently against the US dollar over decades. From 2000 to 2024, the rupee fell from approximately ₹45 to ₹83 per dollar, a depreciation of over 80%. By holding global assets (especially USD-denominated), you create a natural hedge against further rupee depreciation.

Building Your Global Portfolio

Portfolio construction is not a one-time exercise but a continuous journey of alignment between your financial goals, risk capacity, and market opportunities. The framework we've outlined provides a robust starting point:

- Identify your investor persona based on time horizon, goals, and genuine risk tolerance

- Establish your strategic asset allocation across equities, fixed income, and alternatives

- Dedicate 20-30% of your equity allocation to global markets to break free from home bias

- Implement through low-cost, tax-efficient vehicles appropriate to your situation

- Rebalance systematically and stay the course through market cycles

Remember, India represents just 4% of global market capitalization. While India's growth trajectory is exciting and worthy of meaningful allocation, limiting yourself to this 4% means missing out on 96% of global investment opportunities.

A well-constructed global portfolio is your best defense against uncertainty and your most powerful tool for long-term wealth creation. It's not about predicting which country will outperform, it's about ensuring you participate in global growth wherever it occurs, while managing risk through intelligent diversification.

The world is your investment universe. It's time to build a portfolio that reflects that reality.

Disclaimer

This article is intended for information only and does not constitute investment, tax, or legal advice. The material is based on public sources and our interpretation of current market conditions, which may change. Investing in global markets entails risks, including currency risk, political risk, and market volatility. Please seek advice from qualified financial, tax, and legal professionals before acting.